Home Buyer Blunders.

Don't lose a home by making these common homebuying mistakes.

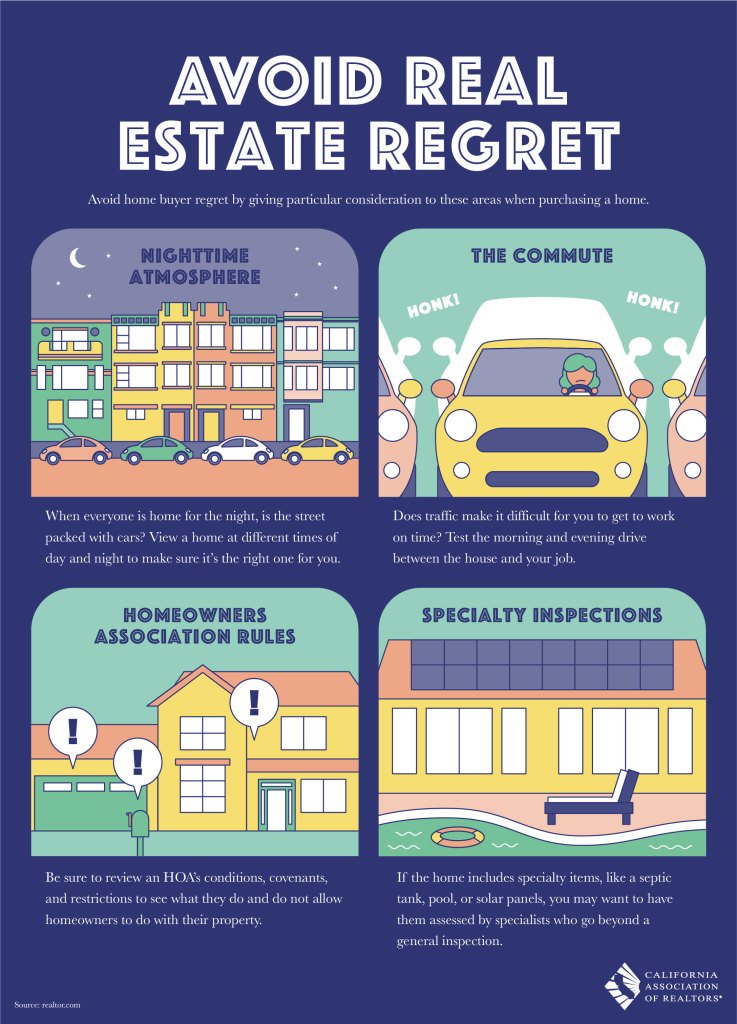

Avoid real estate regret.

Will you still love your new home tomorrow? Four tips to minimize buyer’s remorse.

So You Want To Buy A House!

Now what?…look, look, look, and get an energetic agent who will become your eyes and ears, your watchdog, your educator. The best agent will be one who is referred by another person who knows that agent. Ask friends, relatives, co-workers.

Does the Agent Cost You Anything?

Maybe...like going to the mechanic, nothing is free. If it is free, it's not likely to be great advise and service. Even free relatives can give you poor advise. I've seen this more than I like, and disappointed buyers can and do lose the property they wanted.

However, the cost, though not free, is negotiable. Your agent will advise you.

Most importantly, you owe your agent your Buyer’s Loyalty. A good agent will protect your best interests and work hard to help you find you a property, without getting paid till you actually buy a house. Interview agents, then decide which one is good for you, and stick with that agent. Build rapport, let the agent really get to know you and your family, so that the agent understands your housing needs.

How Do You Find A House?

There are a lot of questions to be answered first:

- What do you like about the home you are living in now?

- What features would you like to duplicate if possible?

- What must you avoid?

With your agent, you begin to explore neighborhoods to narrow down your search. You will also have worked with your lender to ARRANGE FINANCING IN ADVANCE. When you find your house, you will be ready to make the offer, without having to wait for the financing details. Your offer is much stronger with these details in place.

Your agent will be previewing homes to eliminate the ones that do not fit your criteria, then you will be shown the homes that do fit your criteria. If you spot an interesting house on your own, let the agent know immediately so she can research the property for you and look for red flags in the property details.

But wait! Financing Comes First

In today’s market, serious buyers arrange financing before seeing homes.

You will:

- Meet with a lender

- Review loan options

- Obtain a fully underwritten pre-approval (not just a quick letter)

When the right house appears, you’ll be ready to act immediately.

In competitive Silicon Valley markets, hesitation often means losing the home.

A prepared buyer is a powerful buyer.

Keep An Open Mind!

Putting your first impressions aside, evaluate each property carefully. It’s important to look at the house, not the contents the current owners have. The house may be wonderful, but the furnishings may not suit your style.

Study the neighborhood. Check on schools if needed, traffic patterns at different times of the day, shopping, and anything else that may be important to your lifestyle.

Tell the agent what you are thinking about each property (without letting the current owners hear you!), so that the agent knows your impressions. This is especially important in this century. Many sellers have security systems which allow them to hear what is going on in the house. Do not talk about the house AT ALL, until you leave, or discuss things in whispers. You do not want to give away information which may be critical to your negotiation later.